FI/RE Chapter 1 - Defining The Basics

What is financial independence? How much money do I need to retire comfortably?

What is FI/RE (Financial Independence/Retire Early)?

It is typically defined as having enough income (from investments, passive businesses, real estate, etc.) to pay for your reasonable living expenses for the rest of your life. You have the freedom to do what you want with your time (within reason). Working (full or part-time), hobbies which generate income, or other activities are optional at this point. The basic tenet of FI is to spend less than you earn and invest the difference into things that earn money for you. The core philosophy involves aggressive saving, strategic investing, and intentional living to gain the freedom to leave full-time work decades ahead of schedule.

FIRE Acronyms & Strategies Comparison

The 4% Rule in FIRE and Why Early Retirees Should Avoid This Number

The 4% rule is a fundamental withdrawal strategy in the Financial Independence, Retire Early (FIRE) movement that suggests withdrawing 4% of your total retirement portfolio in the first year of retirement and then adjusting subsequent withdrawals annually for inflation. This model aims to provide a sustainable income stream for approximately 30 years.

Assuming a life expectancy of 95 years, the 4% rule works well for people who plan to retire at the age of 65 (a 30-year horizon). However, for early retirees (those who are looking for a 50-year horizon), this model only has a 36% chance of succeeding.

Therefore, experts suggest a 3% withdrawal rate for longer retirement periods (a 50-year horizon). This translates to targeting 33 times your annual expenses. I personally lean more towards conservatism and set a 3% withdrawal rate goal in my calculations. The significance of this approach lies in the fact that there has never been a single period in US history when the 3% rule has failed.

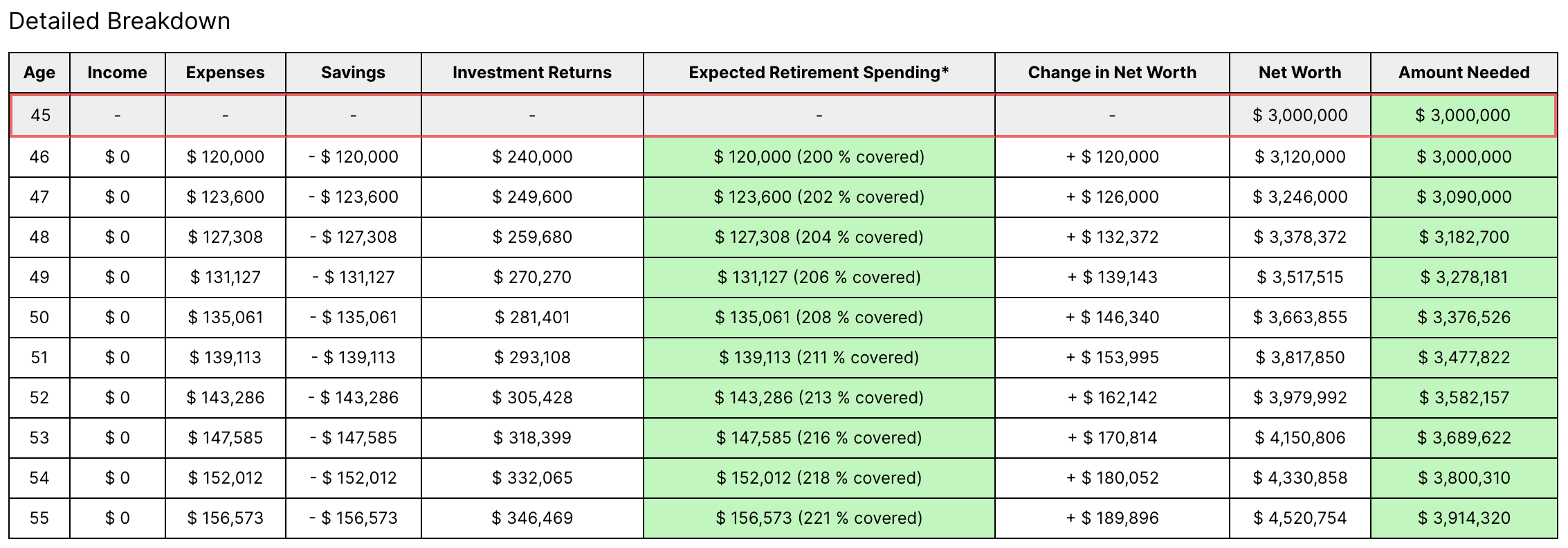

Example

If Sam had invested $3,000,000 in a portfolio averaging 8% annual returns, the 4% rule suggests that Sam can withdraw $120,000 in the first year. This is the only year when Sam calculates 4% of their portfolio. From then on, Sam will base future withdrawals on the amount they withdrew the previous year and adjust them for inflation. Historically, inflation has averaged around 3%. In this case, Sam’s withdrawals would appear as follows:

Year 1 Expenses: $120,000

Year 2 Expenses: $120,000 x 1.03 = $123,600

Year 3 Expenses: $123,600 x 1.03 = $127,308

How much do I need to retire?

Before we delve into the actual amount, let’s make some assumptions.

Family Size: We assume a family size of four and plan for various scenarios, including dual-income single-kid households (DISK), dual-income no-kid households (DINK), single-income households, and individuals.

The FI/RE Corpus calculations all assume Fat FIRE, which represents the highest amount of money needed to maintain a comfortable lifestyle.

Inflation Rate : Typically assumes a 2% annual inflation rate, which is the Federal Reserve’s target. In contrast, historical data in the Indian context suggests an annual inflation rate of around 6%. Withdrawals are adjusted annually to match inflation, thereby preserving purchasing power.

Corpus Growth Rate: This portfolio composition strikes a balance between common stocks and intermediate-term Treasury bonds. Historically, a balanced (60/40) portfolio has delivered an average annual return of approximately 8%.

Health Insurance: In all the calculations below, I’ve specifically excluded the cost of additional health insurance. The primary reason for this is that it can vary significantly depending on an individual’s lifestyle and the specific healthcare plans available in different states. However, I’ll provide an example later in the post to illustrate how much buffer you should have to reach your FI/RE goal if you live in King County, Washington.

FI/RE Corpus Target in USA

The below table offers insights into the size of a corpus required to retire without actively working for a job. I intentionally refrain from specifying values for various FIRE types, as each individual may have their own definition. Therefore, I base this analysis on annual expenditures, which seems more logical in this context.

Factoring in Health Insurance and College Tuition

Health Insurance

Healthcare represents the most significant uncertainty in FIRE planning, particularly in the United States. Upon achieving financial independence, individuals must fully cover health insurance costs, which can be substantial. In Washington State, a United Healthcare Plan plan for a family of three can cost around $1700 monthly, totaling approximately $25000 annually (which includes healthcare premiums, copays, medicine, and out of pocket estimates). Assuming healthcare costs inflate at 3%, an additional $832,000 ($25000 x 33.33) corpus is required to sustainably cover these expenses using the safe withdrawal method.

Future College Expenses

Another goal is to be able to fund 4 years of in-state tuition for your kid. Assuming you have 12-15 years to reach that horizon. University of Washington costs ~$50,000 per year for a 4 year bachelors program. This comes to around ~$200,000 in todays dollar and $320,206 in future value (12 years from now). Using Bank Rate College Savings Calculator and I find that if I had ~$150,000 lump sum right now that should be sufficient enough to cover the full education expense in 12 years (this is roughly an 8% annual return rate).

This means FIRE seekers must strategically account for healthcare and college fees as a critical component of their long-term financial independence strategy, potentially adjusting their total retirement corpus and exploring healthcare exchange options to manage these escalating costs. To summarize, for someone planning to retire in Washington (King County) they would need to add ~$1,000,000 ($832,000 + $150,000) more to their overall FI/RE goal.

Total Breakdown

Healthcare Insurance and College Fee (1 Kid) : ~$1,000,000

Annual Expense: ~$4,000,000

Total Corpus: ~$5M ($4M + ~$1M)

FI/RE Corpus Target Outside USA (INDIA)

This section is tailored for individuals whose ultimate objective is to FIRE outside the United States, preferably in their home country. I’ll provide an example using India, as that’s the country I envision retiring in once I achieve financial independence.

Note: When planning to return to India, Non-Resident Indians (NRIs) can strategically invest their parking funds in US Dollars. Over the past 30 years, the Indian Rupee has consistently depreciated against the US Dollar, losing approximately 5-6% annually. By preserving their wealth in US Dollars, NRIs can safeguard against currency erosion and potentially earn higher returns. For simplicity, I have assumed all values in USD instead of INR to avoid currency fluctuations.

Conclusion

Financial independence (FI) means having enough income from investments to cover living expenses for life, allowing for freedom in time management. Achieving FI requires aggressive saving, strategic investing, and intentional living.

The 4% rule proves robust for traditional 30-year retirements, while 3% serves as a conservative baseline for extended retirement horizons (50-year horizon).

Regions with a higher cost of living necessitate significantly larger retirement savings. The savings corpus grows proportionally to annual expenses.

Healthcare Insurance and College Fees are the most significant uncertainties in FIRE planning, especially in the United States. For individuals planning to achieve FIRE in the US, these factors must be carefully considered and factored into their planning, as they vary significantly from state to state based on the healthcare plans offered.

Disclaimer: The information provided on this blog is for informational and educational purposes only. It should not be construed as professional financial advice. I am not a certified financial advisor, accountant, or financial professional.

References

https://www.investopedia.com/terms/f/four-percent-rule.asp

https://www.madfientist.com/safe-withdrawal-rate/

https://www.schwab.com/learn/story/beyond-4-rule-how-much-can-you-spend-retirement

https://www.investopedia.com/terms/s/safe-withdrawal-rate-swr-method.asp

https://mf.nipponindiaim.com/mutual-fund-articles/4-percent-rule

https://www.vanguardmexico.com/content/dam/intl/americas/documents/mexico/en/fuel-for-the-fire.pdf

https://www.wahealthplanfinder.org/us/en/my-account/savings-options/cascade-care-savings.html